By Joseph Bryson November 7, 2025

The B2B commerce landscape has been undergoing a major shift as digital platforms redefine how suppliers and buyers transact. While consumer eCommerce has long relied on “buy now, pay later” models to increase conversion, the B2B sector is only recently catching up. Adding net terms at checkout is no longer a nice-to-have; it is becoming a competitive differentiator that directly impacts conversion rates, average order value, and long-term customer relationships. Businesses are realizing that integrating B2B payments and extending trade credit digitally can simultaneously improve buyer experience and accelerate cash flow for sellers. The emergence of buy now pay later for business models is bridging the long-standing gap between traditional credit systems and modern digital transactions, offering both flexibility and security at scale.

In this context, B2B Pay Later platforms are transforming how companies approach trade credit. By embedding net terms and invoice financing into online checkouts and invoicing systems, suppliers can offer instant purchasing power to customers without assuming credit risk. Buyers get the freedom to manage cash flow and pay later, while sellers get paid upfront. This dual benefit has made BNPL for businesses one of the fastest-growing innovations in financial technology for B2B trade.

Understanding the Evolution of B2B Net Terms

For decades, trade credit has been the backbone of B2B commerce. Companies have relied on 30-, 60-, or 90-day net terms to build trust and manage purchasing relationships. However, the process was traditionally slow, manual, and reliant on lengthy credit checks and paper-based invoicing. As digital transformation accelerates, businesses are now looking to automate and streamline these processes. The introduction of B2B net terms at checkout represents the digital evolution of this concept. Instead of waiting for human approval or accounting verification, automated systems use real-time credit decisioning to approve buyers instantly.

This automation is largely driven by trade credit platforms that leverage data analytics and embedded B2B payments infrastructure. They eliminate the friction of manual AR management while keeping finance teams reconciled through ERP and invoicing integrations. As a result, businesses can extend credit to more customers, faster, without compromising on risk control. The modernization of net terms is not only improving buyer convenience but also helping sellers expand market reach and improve order efficiency.

How Embedded B2B Payments Drive Adoption

One of the main reasons B2B pay later models are gaining popularity is the rise of embedded financial technology. Embedded B2B payments allow credit, invoicing, and reconciliation to occur within the same workflow, whether it’s through eCommerce portals, ERP systems, or supplier dashboards. This seamless experience reduces the need for manual processing and improves transaction transparency for both parties.

Businesses using embedded systems can integrate payment methods such as ACH transfers, wire payments, and virtual cards, all within the checkout environment. This flexibility caters to different buyer preferences while maintaining efficiency and compliance. When invoice financing and automated collections are added to the mix, suppliers can scale transactions confidently, knowing their cash flow will not be disrupted. This embedded infrastructure is the technological backbone that enables the new generation of BNPL for businesses solutions.

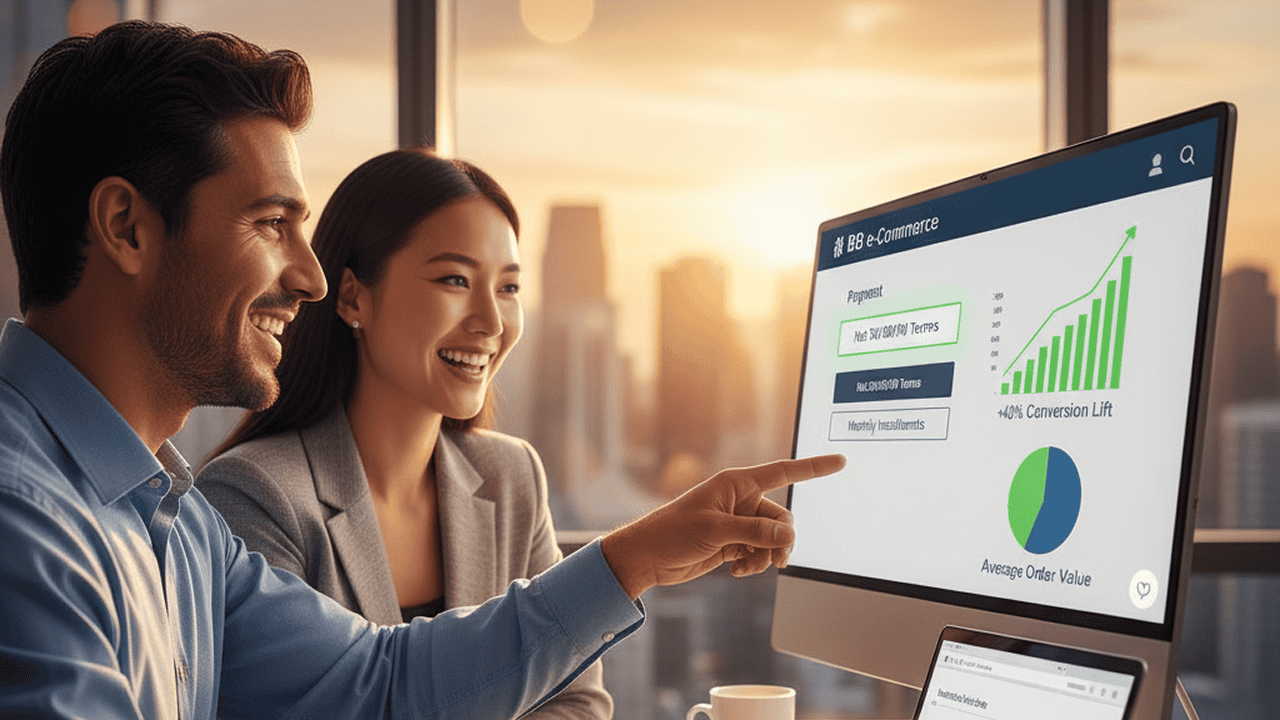

The Conversion Advantage of Net Terms at Checkout

Adding net terms at checkout significantly impacts conversion rates in B2B commerce. One of the primary barriers to online purchasing among business buyers is cash flow constraint. Even when buyers are ready to purchase, they often prefer paying after delivery or upon invoice approval. Allowing B2B pay later options removes this barrier, making it easier for customers to place large orders without immediate financial pressure.

Data from early adopters of B2B payments technology shows that conversion rates can rise by as much as 20 to 30 percent when credit options are visible at checkout. This mirrors the success of buy now pay later for business models in consumer markets, where flexible financing consistently reduces cart abandonment. For suppliers, offering digital trade credit directly in their checkout flow creates a frictionless purchasing journey, encouraging buyers to complete more transactions and deepen loyalty.

Increasing Average Order Value with B2B Pay Later

Beyond conversion, B2B pay later solutions have a direct effect on average order value (AOV). When buyers know they have the flexibility to defer payment, they are more likely to order higher quantities or explore premium products. Traditional net terms achieved this in offline trade, but bringing that same capability to digital checkouts multiplies the effect. Buyers are empowered to align procurement with demand rather than cash on hand, which often leads to larger and more frequent orders.

This phenomenon is amplified when BNPL for businesses integrates with ERP and CRM data, helping suppliers understand purchase patterns and extend personalized credit limits. The result is not only an increase in order size but also a stronger relationship between buyer and seller, where trust is built on transparent payment flexibility. For suppliers, the ability to offer these terms while still getting paid upfront through invoice financing turns credit extension into a growth strategy rather than a risk.

Reducing Risk Through Trade Credit Platforms

One of the biggest challenges in extending credit is managing the associated risk. Historically, sellers were hesitant to offer B2B net terms due to concerns about defaults and delayed payments. Modern trade credit platforms address this by combining automated risk assessment, credit insurance, and real-time monitoring. These systems evaluate buyer creditworthiness instantly using financial data, payment history, and business performance metrics, removing the guesswork from credit decisions.

This approach ensures that suppliers can extend credit safely while maintaining steady cash flow. The platform typically pays the seller upfront and handles collections later, transferring risk from supplier to financier. By integrating these features within embedded B2B payments, businesses can enjoy both protection and agility. The rise of such solutions marks a shift from manual credit management to intelligent, automated systems designed for the speed of digital commerce.

The Role of Invoice Financing in B2B Cash Flow

Cash flow is the lifeblood of any B2B company, and invoice financing plays a pivotal role in maintaining liquidity. When a supplier extends B2B net terms, there is often a delay between shipment and payment. Invoice financing bridges that gap by allowing suppliers to access funds immediately after invoicing, even when the buyer pays later. This capability ensures that operations, payroll, and production remain unaffected by delayed receivables.

By linking invoice financing directly with checkout-based net terms, businesses can automate both the credit offering and the cash advance. This model benefits everyone involved, as the buyer gains flexibility to pay later and the seller avoids the strain of waiting for payments. It’s a practical, scalable solution for modern supply chains where speed and predictability matter more than ever. As more companies digitize their financial workflows, invoice financing has become a standard feature of advanced trade credit platforms.

Enhancing Buyer Experience Through Seamless Credit

Customer experience is becoming a decisive factor in B2B commerce, and payment flexibility is central to it. Offering buy now pay later for business options at checkout transforms the purchasing journey from transactional to partnership-oriented. Buyers feel valued when they can access instant credit without paperwork, phone calls, or long approval cycles. This ease of access often translates into stronger customer retention and positive brand perception.

Moreover, B2B pay later systems with transparent repayment schedules and reminders simplify financial planning for buyers. Combined with automated invoices, credit limits, and integrated communication, the entire process becomes smoother and more predictable. In an era where B2B buyers expect consumer-grade experiences, this seamless credit model positions suppliers as forward-thinking and customer-centric. The improved experience often translates directly into recurring business and long-term loyalty.

Operational Efficiency and AR Automation

Behind the scenes, B2B payments innovation is also reshaping accounts receivable management. Traditionally, AR teams spent significant time reconciling invoices, chasing payments, and updating records. The use of embedded B2B payments and AR automation reduces this burden dramatically. With everything integrated from checkout to invoice settlement, finance teams gain real-time visibility into outstanding amounts and cash positions.

By using platforms like B2B Pay Later, companies can automate reminders, reconcile payments automatically, and link data to ERP systems. This reduces manual intervention and errors, freeing up teams to focus on strategic financial planning. The efficiency gains contribute not just to cost savings but also to better compliance and audit readiness. For organizations processing thousands of transactions, the combination of automation and accuracy becomes a core competitive advantage.

How B2B Pay Later Fits into Digital Transformation

The digital transformation of B2B commerce extends beyond storefronts and CRM systems; it now includes financial workflows. Implementing B2B pay later options is part of this larger modernization effort. When businesses digitize credit, invoicing, and payments, they achieve end-to-end visibility across their revenue cycle. The ability to connect data from embedded B2B payments, inventory, and customer systems enables smarter decision-making and predictive cash flow management.

This shift aligns with the broader trend toward financial technology convergence, where payment, risk, and operational tools coexist within unified ecosystems. In this environment, trade credit platforms are not standalone utilities but integral components of digital business infrastructure. They help organizations adapt to faster sales cycles, global buyers, and dynamic supply chains, all while keeping financial processes compliant and scalable.

Overcoming Traditional Credit Barriers in B2B Commerce

Despite its advantages, the concept of extending credit has often been hindered by legacy practices. Many suppliers still rely on manual credit vetting or outdated ERP systems that cannot handle real-time approvals. This lag creates friction and missed opportunities, especially in online transactions where speed is crucial. B2B net terms solutions powered by automation solve this by providing instant credit decisions, removing the bottlenecks of traditional credit management.

In industries such as manufacturing, wholesale, and distribution, where order values are high, instant B2B pay later functionality is particularly valuable. Buyers no longer need to wait days for credit approval; they can complete purchases within minutes. Sellers, in turn, can scale sales operations without fearing default risk. This agility is transforming B2B commerce into a faster, more accessible ecosystem for both new and existing customers.

The Strategic Impact on B2B Relationships

While the financial benefits of BNPL for businesses are clear, the strategic impact on customer relationships is equally important. Offering flexible payment terms signals trust and partnership, reinforcing long-term collaboration. Buyers who have access to net terms tend to stick with suppliers who make purchasing easy and reliable. Over time, this mutual trust strengthens supply chain stability and reduces churn.

Furthermore, the data insights generated by embedded B2B payments systems enable suppliers to anticipate customer needs and tailor offerings accordingly. Credit limits can be adjusted dynamically based on order history and payment behavior, fostering personalized financial experiences. The combination of trust, transparency, and technology creates a foundation for deeper, more resilient business relationships that drive growth over time.

Future Trends: AI and Real-Time Credit Decisioning

As technology advances, artificial intelligence is playing a greater role in trade credit platforms. Machine learning models can now assess risk more accurately by analyzing behavioral and transactional data in real time. This allows for dynamic credit limits that adapt to buyer activity, improving both security and accessibility. With AI-driven invoice financing, sellers can predict cash flow gaps before they occur and adjust payment policies proactively.

The integration of AI also enhances fraud detection and compliance monitoring, ensuring that B2B payments remain secure across global transactions. The future of B2B pay later will likely involve even greater personalization, where credit terms are adjusted automatically based on buyer profile and order size. This evolution reflects the broader trend of intelligent automation across financial services and underscores how far B2B commerce has come in digitizing trust.

Why Suppliers Can’t Afford to Ignore Pay Later Models

In today’s digital marketplace, ignoring buy now pay later for business options means losing potential sales to competitors who offer them. B2B buyers increasingly expect the same payment flexibility they experience as consumers. For suppliers, offering B2B pay later terms is not only a sales tool but also a strategic lever for market differentiation. It enables them to serve a wider range of customers, including small and mid-sized businesses that depend on credit to manage cash flow.

Moreover, platforms like B2B Pay Later remove the financial burden by paying suppliers upfront. This means suppliers gain the benefits of extended credit without exposure to non-payment risk. In an era where digital commerce is defined by speed and customer experience, adopting this model ensures that suppliers stay relevant, agile, and financially secure.

Conclusion

Adding net terms at checkout is one of the most effective ways to increase both conversion and average order value in B2B commerce. It modernizes the traditional credit system and aligns it with digital purchasing behavior. With the support of B2B pay later, trade credit platforms, and embedded B2B payments, businesses can unlock new growth opportunities while maintaining financial control. Buyers gain flexibility and trust, and sellers enjoy faster payments and stronger customer loyalty.

The future of B2B commerce lies in intelligent, automated, and inclusive payment models that balance risk with opportunity. Integrating invoice financing, real-time credit decisioning, and seamless embedded payment flows will define the next phase of B2B digital transformation. For companies looking to grow their online sales and build lasting customer relationships, offering buy now pay later for business is not just a payment option; it’s a growth strategy.